Industry

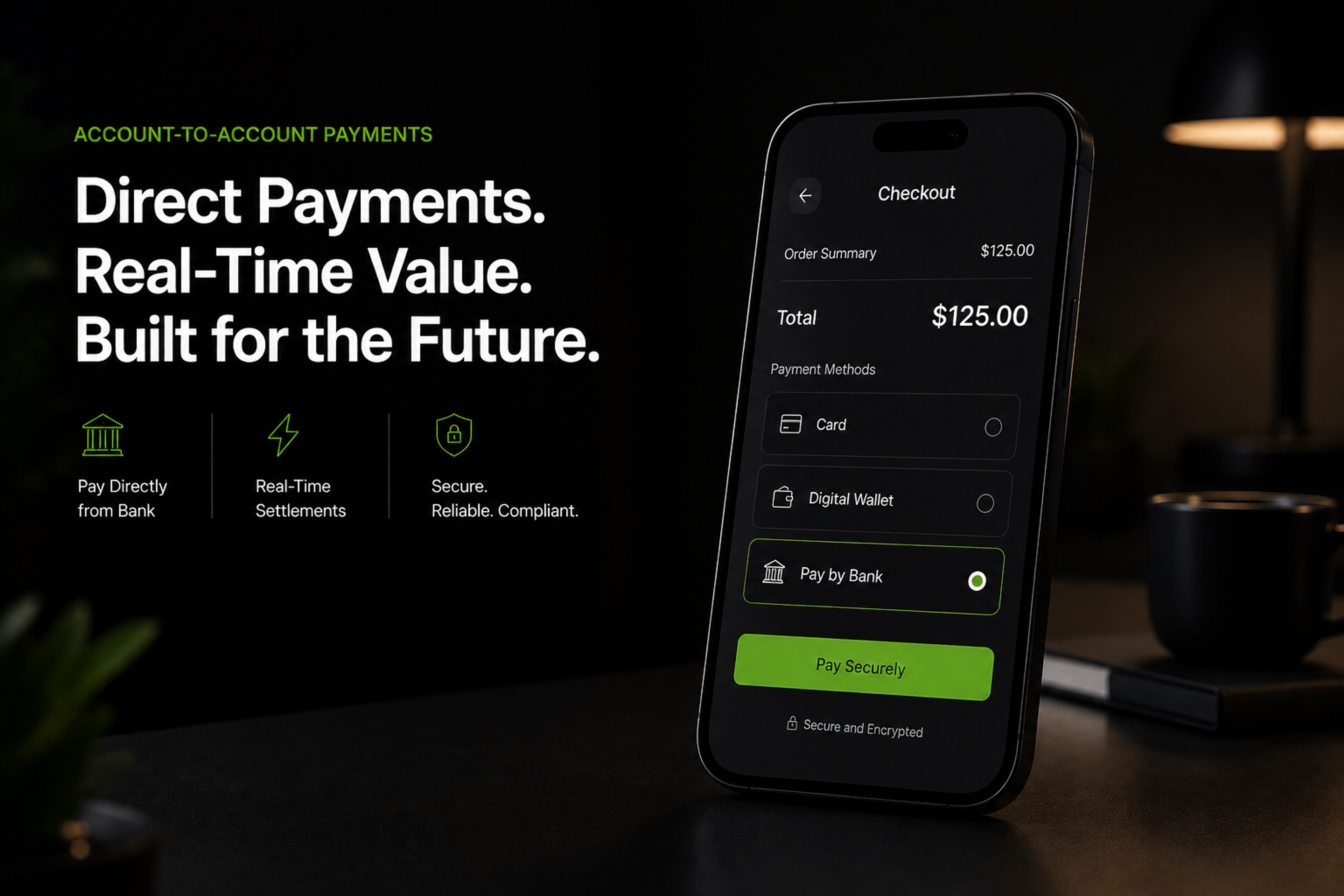

A2A Payments

Building the infrastructure for account-to-account payments — open banking, instant payment rails, PSD2 compliance, and fraud-resilient APIs.

Account-to-account payments — money moving directly between bank accounts without passing through a card network — are the fastest-growing segment of European payments. They sit at the intersection of two regulatory waves: open banking, which forced banks to expose payment-initiation APIs under PSD2 and the UK's CMA mandate; and instant payments, which the EU's Instant Payments Regulation (in force from 8 April 2024) is making the default credit transfer rail across the SEPA zone.

For payment institutions, banks, and merchant-facing PSPs, the engineering reality is denser than the regulation suggests. Open banking implementations vary widely across ASPSPs even within a single standard. APP fraud reimbursement — mandatory in the UK from 7 October 2024 with an £85,000 cap and 50/50 PSP liability — has shifted the economics of fraud control. Verification of Payee, mandatory under the IPR from 9 October 2025, mustintegrate cleanly into every SEPA credit transfer without breaking the conversion advantage that makes A2A worth pursuing.

Digital Bank Expert helps Payment Institutions, EMIs, banks, and acquirer-PSPs build A2A capability end-to-end: PISP and AISP integration across UK and EU bank coverage, Berlin Group / Open Banking UK normalisation, real-time fraud and APP-reimbursement infrastructure, IPR-compliant SEPA Instant connectivity, Verification of Payee, andFCA/EBA-grade evidence packs. Every engagement is led by senior consultants who have shipped open banking and instant payments platforms for regulated UK and EU institutions.

Industry Challenges

Open Banking API Complexity

Building reliable, secure, and standards-compliant PIS and AIS integrations across multiple banks and markets.

Fraud in Faster Payments

The speed of instant payments removes the window for traditional fraud controls — requiring real-time ML models.

Regulatory Fragmentation

PSD2, PSD3, and national instant payment regulations vary across EU markets, requiring multi-jurisdiction compliance.

Merchant Adoption

Driving merchant uptake requires seamless UX and clear commercial models compared to card alternatives.

Our Solutions

API-First A2A Integration

Payment Initiation Services, Account Information Services, multi-currency, and recurring payment APIs.

Real-Time Fraud Prevention

SCA, ML-powered transaction monitoring, encryption, tokenisation, and PSD2/AML/KYC compliance.

High-Volume Performance

Engineered for high-volume, low-latency instant payment processing with 99.99%+ availability.

Multi-Market Compliance

PCI DSS, PSD2/PSD3, AML, and KYC across UK, EU, and international markets.

A2A payments by the numbers

Frequently asked questions about A2A payments

Services We Provide

Solution Design

Technical architecture for regulated financial institutions — the bridge between strategy and implementation. Integration architecture, data design, security and compliance built in, and non-functional requirements specified to the level engineering can actually build from. Vendor-neutral across the platform stack; senior architects with hands-on production experience.

Custom Rust Development

Rust development for the integration layer of banks and fintechs — ISO 8583 and ISO 20022 message processing, payment routing, and the components where memory safety and predictable performance map directly to operational concerns. A focused capability for the parts of the banking stack where Rust earns its place.

Relevant Expertise

Let's solve your A2A Payments challenges

Talk to our specialists about your requirements.

Contact us